Have you ever wondered how taxes work in the United States? Taxes are essential to the functioning of the country, but their system can seem complex and varied depending on the type of income, status, or immigration status. In this article, we’ll break down in detail what taxes are, the different types that exist, and how they impact citizens, residents, and immigrants alike.

What are taxes in the United States?

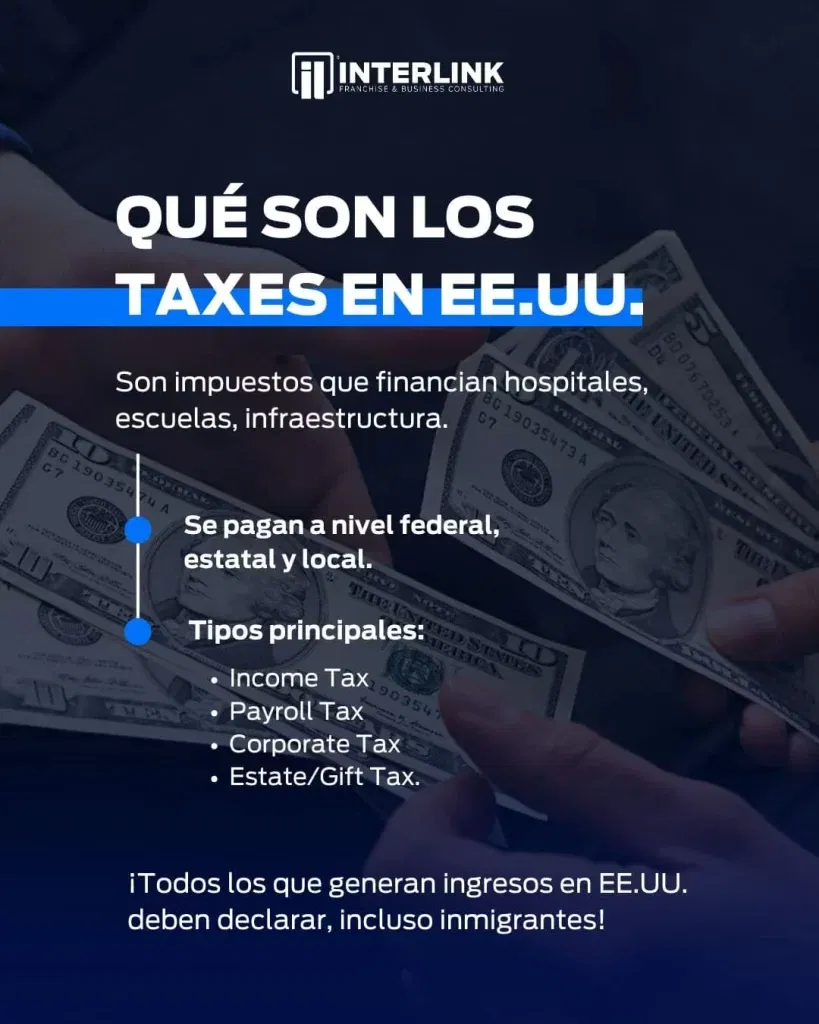

Taxes are mandatory taxes that individuals, businesses, and other entities must pay to different levels of government (federal, state, and local). These taxes constitute the government’s main source of revenue to finance public goods and services. Some examples of what they fund include roads, hospitals, schools, the military, and social programs like Medicare and Social Security.

Interesting fact: The United States has a progressive and decentralized tax system, which means that tax rates and types vary depending on taxpayers’ income and geographic location.

Each state is free to impose its own taxes, in addition to the federal taxes set by the central government.

Why it’s important to understand the tax system

Understanding how taxes work not only allows you to comply with your legal obligations, but also to optimize your personal or business finances. This includes taking advantage of deductions, tax credits, and avoiding penalties.

Types of taxes in the United States

Federal taxes

These are taxes collected by the federal government and administered by the Internal Revenue Service (IRS). Among the most common are:

Income Tax

The Income Tax or income tax is applied to the income that individuals and legal entities generate annually. This tax has progressive characteristics, that is, people with higher incomes pay a higher percentage. For example:

A person earning $40,000 a year can pay a rate of 12%. Another who earns $500,000 may be in the range of 35% or more, depending on deductions and tax credits.

Companies are also subject to this tax on the net profits they generate, after allowable deductions such as wages, production costs, and employee benefits

Payroll Taxes

Payroll Taxes are mandatory contributions deducted directly from employees’ wages. These taxes fund two essential social programs in the United States: Medicare, which provides health care to people over the age of 65, and Social Security, which offers pensions and disability benefits.

Both employees and employers must contribute a proportionate share of wages to Social Security (6.2%) and Medicare (1.45%). In total, workers see 7.65% of their gross salary withheld for this purpose.

Social Security has a maximum limit on taxable income (in 2024, about $160,200). Once this limit is reached, additional income is no longer subject to this tax.

Thanks to these taxes, millions of seniors and disabled people receive monthly benefits, and active employees accumulate credits for their future retirement.

Corporate Tax

The Corporate Tax taxes the net profits of companies, which means that it is applied on their income after deducting expenses such as salaries, production costs, investments in infrastructure, and social benefits.

Currently, the federal rate for corporate tax is 21% on net profits. However, some companies pay less thanks to tax deductions or government incentives to encourage investment in research, development or infrastructure.

In addition to the federal tax, some states impose additional rates, which can range from 3% to 12%.

This tax is a key source of revenue for the government, but it can also influence investment and business expansion decisions. For example, many businesses look for locations with lower rates or tax incentives.

Estate and Gift Tax

Inheritance and gift tax applies to the transfer of property, either by inheritance upon a person’s death or as a gift during their lifetime.

In 2024, estates that exceed $12.92 million per person are subject to this tax at the federal level. Rates can range from 18% to 40% depending on the value of the inheritance. For gifts, the annual exempt limit is $17,000 per recipient.

Many people turn to legal strategies, such as trusts, to minimize the impact of this tax and protect the value of their assets for their heirs.

Bear in mind: Spouses are usually exempt from paying taxes on inheritances or gifts between them, and donations to charities are also tax-free.

State and local taxes

In addition to federal taxes, each state and locality can impose its own taxes, resulting in a variety of levies such as:

- State Income Taxes: Some states like Florida or Texas don’t have this tax, while others like California apply rates of up to 13.3%.

- Sales Tax: These are indirect taxes applied to the consumption of goods and services, with rates ranging from 4% to 10%.

- Property taxes: They tax the value of real estate and are a key source of revenue for local governments.

Who pays taxes in the United States

In the United States, tax obligations fall on any person or entity that generates income within the country, regardless of their nationality, residency, or immigration status. The following are the main groups that are required to pay taxes:

1. Citizens and legal residents

All U.S. citizens and lawful permanent residents (Green Card holders) are required to report and pay taxes on their global income, i.e., income generated both inside and outside the United States. This rule includes wages, business profits, investments, rents, and any other income.

2. Nonresident aliens with U.S. income

Nonresident aliens who earn income in the U.S., such as wages from temporary jobs, investment income, property rentals, or business profits, must comply with their tax obligations. The government uses a specific formula to determine how much of the income is taxable.

3. Self-employed workers, employees and companies

Both employees and self-employed workers are subject to the payment of taxes. Self-employed workers, in addition to declaring their income, must cover additional taxes such as the Self-Employment Tax, which includes Social Security and Medicare contributions. Companies, on the other hand, must pay Corporate Tax for the net profits they generate.

Do immigrants pay taxes in the United States?

Yes, immigrants, both documented and undocumented, are required to pay taxes if they generate income within the country. This inclusive tax system has several notable features:

Immigrants with legal documents

Immigrants with legal status, such as work visa holders, international students on F-1 or J-1 visas, and permanent residents, must comply with the same tax obligations as U.S. citizens.

Immigrants without legal documents

Even those who do not have a regular immigration status can comply with their tax obligations. These taxpayers can report income using an ITIN (Taxpayer Identification Number) instead of a Social Security Number (SSN). The ITIN is issued by the Internal Revenue Service (IRS) and allows these individuals to comply with tax law in a legal and transparent manner.

Paying taxes can be a valuable tool for immigrants, because:

- Demonstrates roots in the country: Complying with tax obligations can serve as evidence of residency in future immigration applications.

- Contributes to the economy: Immigrants contribute billions of dollars annually in federal, state, and local taxes, supporting social programs like Social Security and Medicare.

- Encourages regularization: Tax history can be a key requirement in certain immigration regularization processes.

What are taxes for in the United States?

Taxes are essential to maintaining the functioning of government and the provision of public services. Finance:

- National Security and Defense: Military budget.

- Public health: Programs like Medicare and Medicaid.

- Education: Grants for public schools and universities.

- Infrastructure: Roads, bridges and public transport.

- Social security: Payments to retirees and the disabled.

How taxes work in the United States

Automatic Holds

For employees, the employer automatically deducts taxes from each paycheck. This includes federal income tax, state taxes (if any), and payroll taxes.

Quarterly Payments

Self-employed individuals, contractors, and businesses that do not have automatic withholding must make estimated payments to the IRS each quarter (in January, April, June, and September). This ensures that they do not accumulate tax debts at the end of the tax year.

Annual returns

All taxpayers must file an annual return during the tax season to figure out exactly how much they must pay or if they are entitled to a refund. This return includes income, deductions, and applicable tax credits.

When are taxes paid in the United States

The tax year in the United States usually ends on December 31. From that date, taxpayers have until April 15 of the following year to file their tax return. However, if this date falls on a weekend or national holiday, the deadline is automatically extended to the next business day.

For example:

- If April 15 falls on a Sunday, the deadline will be Monday, April 16.

- In cases of emergencies, such as natural disasters, the IRS may grant additional extensions for affected areas.

Quarterly Estimated Payments

Some taxpayers, such as self-employed individuals, entrepreneurs and those with significant income who do not have taxes withheld directly from their income, must make advance payments to the IRS on the following key dates:

- January 15

- April 15

- June 15

- September 15

Each payment covers one quarter of the fiscal year. For example, the payment made on April 15 corresponds to the first quarter of the year. Failure to meet these deadlines can result in late payment penalties, even if the annual return is filed on time.

Time extensions

If you can’t file by April 15, you can request an extension from the IRS, which will give you until Oct. 15 to complete the filing. However, it is important to remember that the extension only applies to the submission of the return, not to the payment of taxes owed. If you don’t pay what you owe by April, interest and penalties may apply.

How taxes are done in the United States

Doing taxes in the United States may seem complicated, but following an organized process can make it easier. Below, we explain the essential steps to comply with this tax obligation:

1. Gather the necessary documentation

Before you begin, make sure you have all the documents required to prepare your return. Some of the most common include:

- Forms W-2: Issued by employers, they itemize your income and tax withholdings.

- Forms 1099: These include additional income such as self-employment, investments, bank interest, among others.

- Documentation of deductions and credits: Receipts for medical expenses, mortgage interest, charitable donations, education costs, etc.

- Social Security number (SSN) or ITIN for you and your dependents.

2. Choose how to file taxes

You have two main options for doing your taxes:

- On your own: Using specialized software such as TurboTax, H&R Block or TaxAct. These tools guide the process step-by-step and offer virtual assistance.

- Hire a professional: A CPA or certified tax preparer can be a big help if your finances are complex or if you have income from multiple sources.

3. Determine your filing status

This depends on your personal situation, such as whether you are single, married, have dependents, etc. Your filing status affects the amount of tax you pay and the deductions you’re entitled to.

4. Fill out the right form

Most taxpayers use Form 1040. However, additional schedules may be necessary depending on your income and specific deductions.

5. File the return

You can submit your tax return electronically through the IRS or by physical mail. Electronic filing is faster and reduces errors, as well as speeding up any refund.

6. Pay taxes or claim refunds

If you owe additional taxes, make the payment by April 15 to avoid interest and penalties. On the other hand, if you’re eligible for a refund, make sure you enter your bank account details correctly to receive direct deposit.

U.S. Tax Refund

A positive aspect of the U.S. tax system is the ability to get a refund if you’ve paid more taxes than you were entitled to. This occurs when your withholding during the tax year or the tax credits applied exceed your tax liability.

1. When is a refund generated?

A refund occurs in situations such as:

- Excessive withholdings from your wages during the year.

- Application of deductions and tax credits that reduce your taxable income. For example, the Child Tax Credit or the Earned Income Tax Credit (EITC).

2. How to track your refund

Once you file your return, the IRS allows you to track the status of your refund using the “Where’s My Refund?” tool available on its website or app. You must provide your SSN or ITIN, filing status, and exact amount of expected refund.

3. Processing times

- If you filed electronically: Refunds are usually processed within 21 days.

- If you sent by physical mail: It can take 6-8 weeks or more.

4. Reception Options

You can choose to receive the refund via direct deposit into your bank account, check in the mail, or even apply it as a credit toward next year’s tax payment.

5. Common mistakes to avoid

To make sure you receive your refund without delay:

- Verify that all personal and bank details are correct.

- Be sure to include all the necessary documentation.

- Correct any errors quickly if the IRS notifies you.

Not only does meeting tax calendar dates avoid penalties, but it also ensures that you keep your finances in order and in good standing with the government. Do you have questions about your tax obligations or need personalised advice? Contact us to get in touch with tax professionals.